Close enterprise deals faster by including probabilistic sensitivity analysis in your business case

CFOs view business case projections with healthy skepticism. They've approved too many initiatives where promised ROI never materialized. Single-point forecasts like "projected 250% ROI" trigger eye rolls because no one can predict the future with that precision.

The solution isn't more debate about which assumptions are correct. It's shifting the conversation from defending a single outcome to showing the range of probable outcomes with their likelihoods.

Based on experience evaluating hundreds of business cases for CFO approval, here's how sensitivity analysis builds confidence instead of raising objections.

Key Takeaways

- Static sensitivity analysis (low/expected/high scenarios) doesn't show probability of outcomes

- Probability-based analysis answers "What's the likelihood of achieving target ROI?" not just "What's possible?"

- Use assumption ranges instead of debating perfect point estimates to save time and show transparency

- Automated probability analysis identifies which 1-2 assumptions actually matter, eliminating wasted refinement

Why CFOs Remain Skeptical Despite Sensitivity Analysis

Business cases predict the future. CFOs know that anyone asking for money has bias. They want approval. Sales teams enabling champions naturally present optimistic cases. This built-in skepticism means CFOs smell "too good to be true" from miles away.

A CEO of a $4B company, who served as CFO for years, recently said: "I've never seen a good business case." That's the reality AEs and champions face.

The CFO's job isn't just saying yes or no. It's managing company capital as a steward. They need confidence to act. When business cases lack accuracy that confidence evaporates, even if strategic alignment, practicality, and credibility all check out.

The Problem With Static Sensitivity Analysis

Most business cases use static sensitivity analysis: calculate three scenarios (pessimistic, base, optimistic) with different assumption values. This table looks familiar:

This approach is incrementally better than a single forecast. But it doesn't answer the CFO's critical question: "What's the likelihood of each outcome?"

Is there a 90% chance you hit the worst case? A 10% chance? Without probabilities, the CFO can't assess risk properly. You've just given them three numbers to debate instead of one.

Static analysis also triggers endless debates about assumption values. Sales thinks productivity gains will be 60%, but the champion wants to use 25% to be conservative. Hours get wasted arguing over the "right" number while the deal stalls.

Probability-Based Sensitivity Analysis: The CFO-Ready Approach

Advanced business case platforms use probability-based analysis that transforms how CFOs evaluate risk. Here's how it works:

Use ranges instead of point estimates. Rather than debating whether productivity gains should be 25% or 35%, input a range: 25-35%. No need to find the perfect number. This saves time on data requests and eliminates unproductive debates.

Run automated simulations. The platform runs thousands of calculations, randomly selecting values within your assumption ranges to calculate all potential outcomes. This happens in seconds using advanced statistics, so users don't need to understand the math.

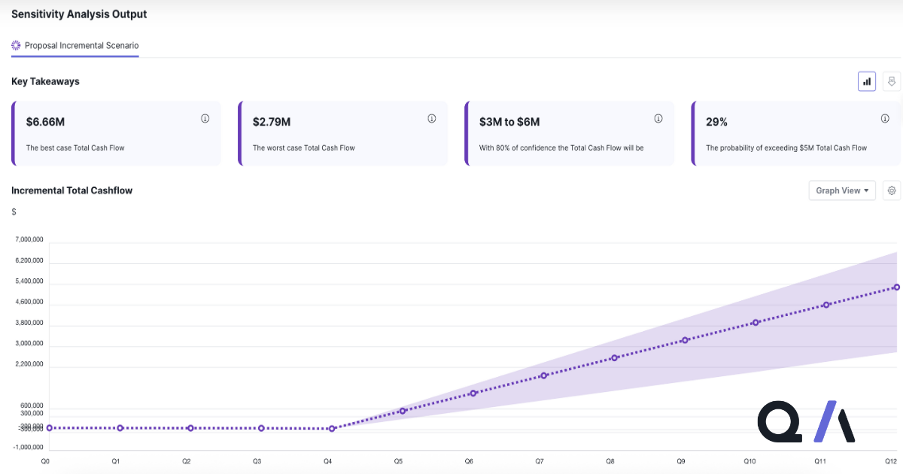

Get probability distributions. Results show best case, worst case, and the probability of achieving specific targets. For example: "With 80% confidence, incremental value will be $3M to $6M" or "29% probability of exceeding $5M in total cash flow."

This approach addresses the accuracy dimension of CFO evaluation by showing not just what could happen, but how likely each outcome is. Even your worst-case scenario might be good enough for approval, and now the CFO knows the odds of hitting it.

How Probability Analysis Changes The Conversation

Probability-based sensitivity analysis shifts discussions from approval debates to optimization conversations.

From: "Will we hit 250% ROI?"

To: "How do we increase the probability of exceeding $5M in value?"

Now you're discussing how to eliminate risks, accelerate timelines, add support resources, or adjust implementation approach.

The analysis also reveals which assumptions actually drive outcomes. Often, the most debated assumption isn't even sensitive. Changing its value barely impacts ROI. You save time refining only the 1-2 assumptions that matter, not all 10.

Everything remains transparent for the CFO to see. No questioning "the math"; it's calculated reliably every time, not with a bespoke spreadsheet that may contain errors.

Static vs. Probability-Based Sensitivity Analysis

Implementing Probability-Based Sensitivity Analysis

Most AEs and champions can't build probability-based sensitivity analysis manually. It requires statistical expertise and specialized software. Attempting it in spreadsheets leads to errors that undermine credibility.

Professional business case platforms automate this analysis. Qarar, built by CFO consultants who evaluated hundreds of business cases, generates probability distributions in seconds using Monte Carlo simulations. Users input assumption ranges and the platform handles the complex statistics.

Start with 3-5 key assumptions that have the most uncertainty. Don't worry about getting perfect ranges initially. As the analysis reveals which assumptions are most sensitive, you can refine those specifically rather than wasting time on assumptions that barely impact outcomes.

When presenting to the CFO, lead with probability statements: "With 80% confidence, we'll achieve $3-6M in incremental value" rather than "We project $4.5M in value." This frames the conversation around likelihood, not defending a single number.

This approach addresses the accuracy dimension that's critical to CFO evaluation. Combined with credibility (hard benefits), practicality (realistic execution), and strategic alignment (on-strategy), probability-based sensitivity analysis completes a CFO-ready business case.

.png)